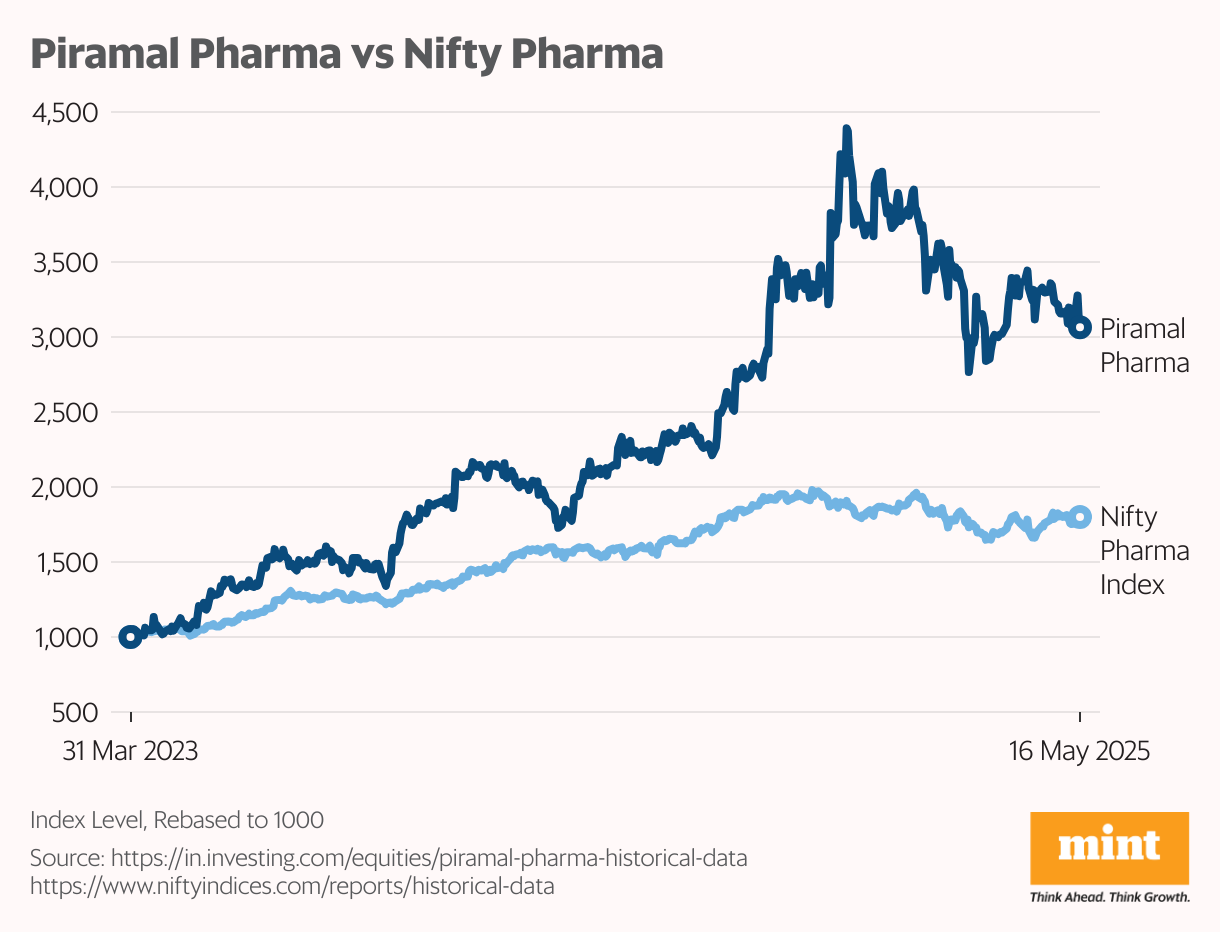

Already weighed down by global policy uncertainty, the Piramal Pharma counter has extended its correction after its earnings for the fourth quarter of 2024-25 disappointed investors.

But is the correction an opportunity for investors to buy the stock, or a signal of more stress to come?

From turnaround to disappointment

Piramal Pharma is one of India’s leading pharmaceutical companies with 17 manufacturing and development sites, and commercial presence in more than 100 countries. Its spick-and-span quality track-record speaks for itself—the company has successfully cleared almost 50 inspections of its global facilities by the US Food and Drug Administrator since FY12.

Piramal Pharma’s financials had been under stress but the company turned around its business. From FY23 to FY25, its revenue grew at a compound annual growth rate of 14%, and its EBITDA margin expanded from 12% to 17%.

And from a loss of ₹186 crore in FY23, Piramal Pharma swung to a profit of ₹91 crore in FY25. Importantly, the turnaround was accompanied by a moderation in debt—net debt to EBITDA dropped from 5.6x to 2.7x during the period.

But Piramal Pharma’s latest fourth-quarter results disappointed investors. Revenue growth was muted at 8% year-on-year and EBITDA margin was flat at 22%. While profit increased 52%, a bulk of the growth was due to a rights write-off undertaken in the base quarter.

Also read | Defence stocks are soaring again, but can fundamentals support the rally?

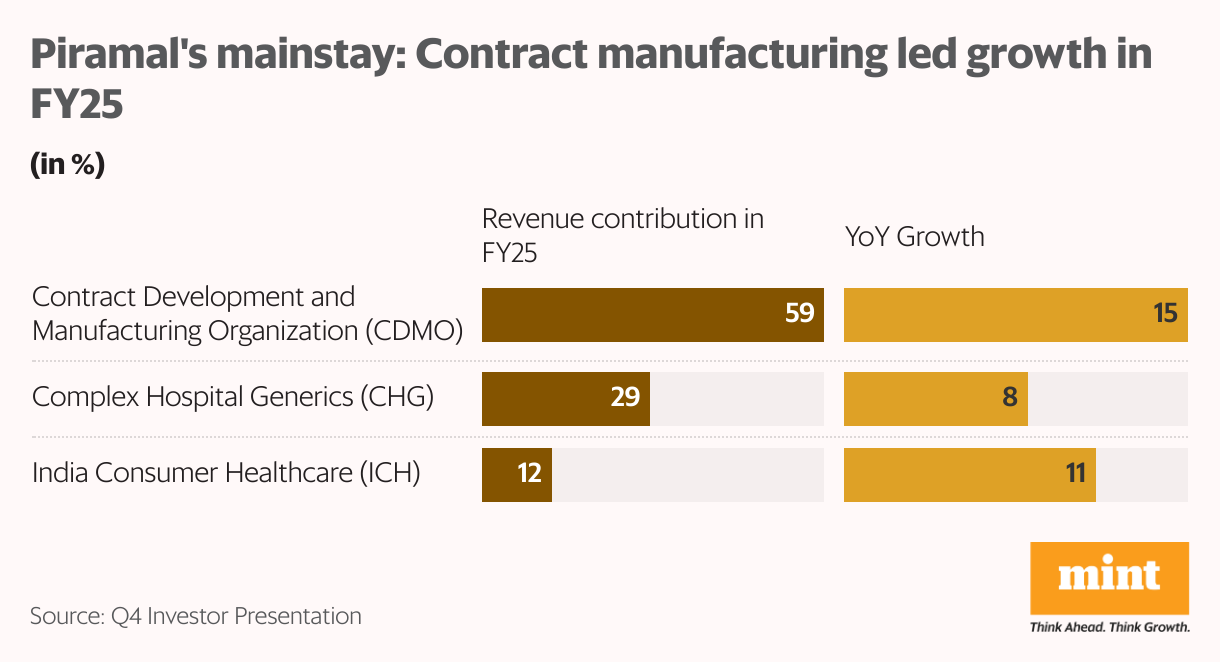

Mainstay segment led growth in FY25

Piramal Pharma operates in three key segments. Its contract development and manufacturing organization (CDMO) business contributed 59% of its revenue in FY25 and its complex hospital generics (CHG) business, which includes products such as anesthesia and intrathecal therapy, accounted for 29%. The balance 12% contribution came from its India consumer healthcare (ICH) business, which deals in over-the-counter consumer and wellness products.

Piramal Pharma’s mainstay segment, CDMO, registered a slightly higher share of innovation-related work last year—54% in FY25 vs 50% in FY24. It also scored a 54% surge in on-patent commercial manufacturing.

The result: The company’s CDMO business delivered 15% year-on-year growth in FY25, supporting overall revenue growth of 12%. EBITDA margin for the segment also improved, thanks to improved efficiencies in procurement and operations.

The tariff uncertainty effect

Pharmaceuticals are currently not under the purview of the US’s reciprocal tariffs on products exported to the country. But US President Donald Trump has indicated that discussions are underway to strip the pharma sector of this exemption.

If that happens, it would significantly hurt India’s pharma sector, which counts the US as its biggest market for pharmaceutical products manufactured in India, including generic or off-patent drugs and pricier branded products.

Indian pharma companies will face steeply higher production costs if they have to move their manufacturing to the US as a result of Trump’s reciprocal tariffs, which have been suspended until 9 July.

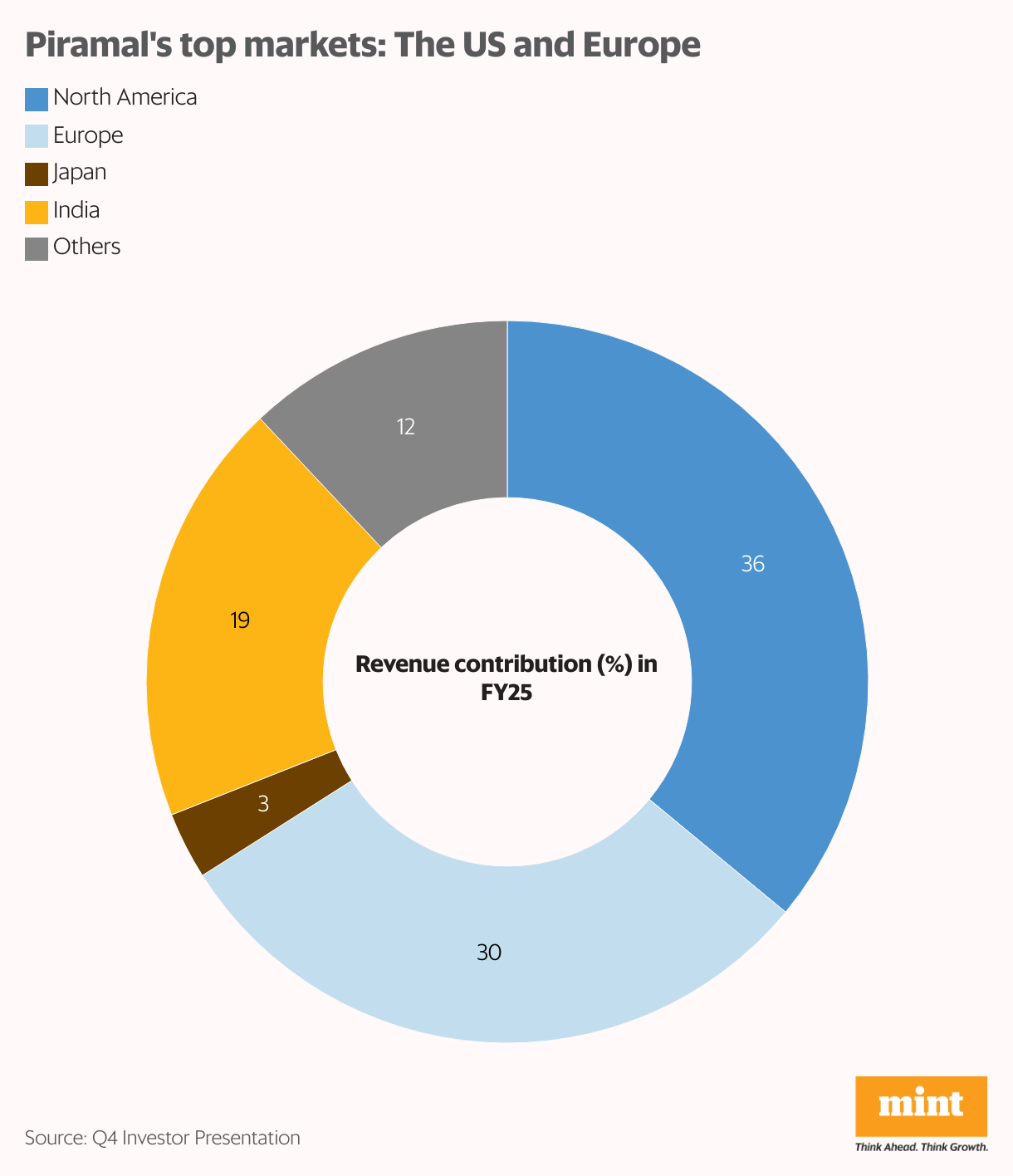

Piramal Pharma, which derives more than a third of its revenue from North America, has already invested $470 million in its manufacturing facilities in the US. Additional capital expenditure of $90 million is in the works.

Also read | Why Tata Teleservices is drawing institutional bets despite mounting losses

Making matters worse: Trump’s drug-pricing order

Despite higher manufacturing costs in the US, higher prices of on-patent drugs in the market could have made manufacturing such products there financially feasible.

But the latest twist in the tale is Trump’s executive order asking pharma companies to slash the prices of on-patent drugs in the US to match the cheapest global prices.

Also read | Mint Explainer: Why Indian pharma is spooked by Trump’s latest drug policy

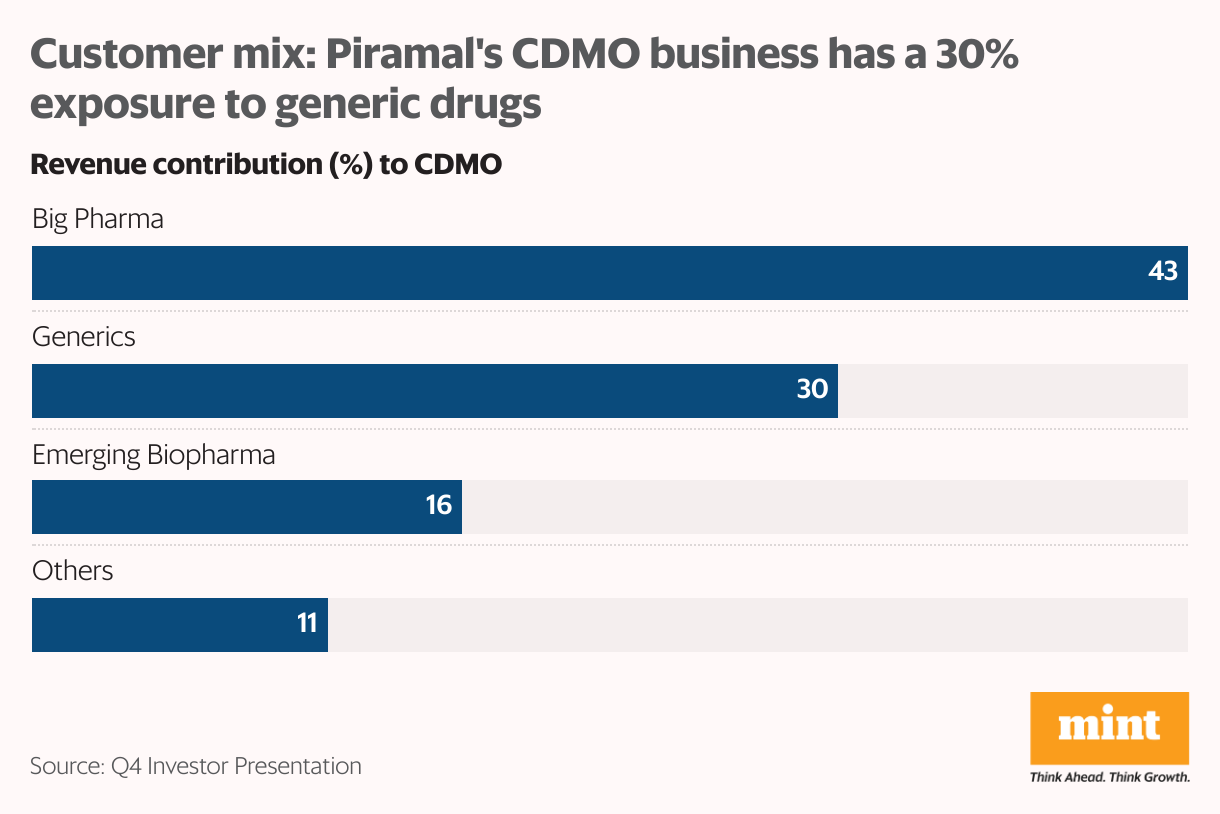

Given that Piramal’s CDMO customer-mix is skewed towards big pharma and emerging biopharma, with only 39% exposure to generics, the company is at risk if Trump’s drug price order goes through.

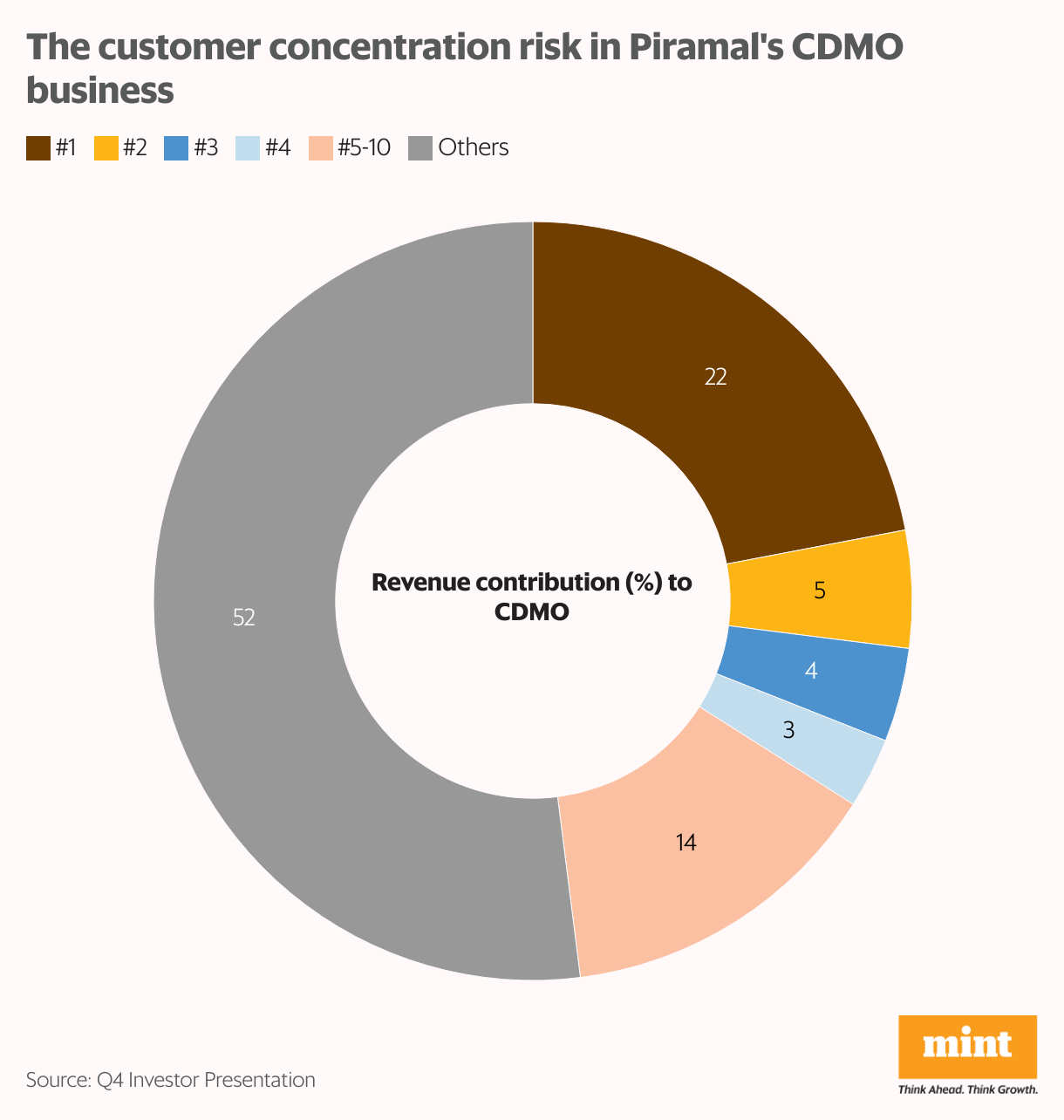

The uncertainty has frayed investors’ nerves. Biotech funding in the US has seen uneven improvement, leading to selective and delayed order placement. The customer concentration risk at Piramal’s CDMO business has exacerbated the circumstances. While it has over 500 customers, its top 10 customers contribute almost half of the business.

Consequently, Piramal’s overseas CDMO sites are operating significantly below capacity. This has reduced operating leverage even as operating expenses rise on account of a new manufacturing facility. Revenue growth in CDMO for Piramal is expected to be in single digits in FY26, with EBITDA margin likely to remain stressed.

Also read | Chalet Hotels is gearing up for a major expansion. Should investors check in now?

India business offers comfort

Piramal Pharma’s CDMO sites in India contribute 6% to its business, and have been operating at healthy utilizations.

The company’s India consumer healthcare (ICH) business has also matched pace with overall growth, registering an 11% increase in revenue. Driven by 52 new products and stock-keeping units (or product lines) launched in FY25, the ICH business crossed the ₹1,000 crore milestone during the year.

About 49% of Piramal’s ICH business came from power brands such as Lacto Calamine, Little’s, and CIR, helping it post a robust 20% rise in fourth-quarter revenue.

About 21% of the segment’s sales came from e-commerce, which registered an overall 39% year-on-year growth for Piramal Pharma in FY25. This negated a slowdown in Piramal Pharma’s i-range products (i-Pill emergency contraceptive, i-Know home kits for pregnancy and other tests, etc.) brought about by regulatory price controls.

Prospects for inorganic growth remain open as well. While Piramal Pharma has clarified that it won’t be re-entering the domestic prescription formulations business, it may consider acquiring domestic over-the-counter portfolios.

Complex hospital generics: Cautious optimism

Piramal’s CHG segment posted an 8% year-on-year revenue growth in FY25, the slowest among all its segments. It also dragged down Piramal’s overall margin due to one-time expenses and capacity expansion in India. But the facility is now operational and expected to deliver revenues starting FY26.

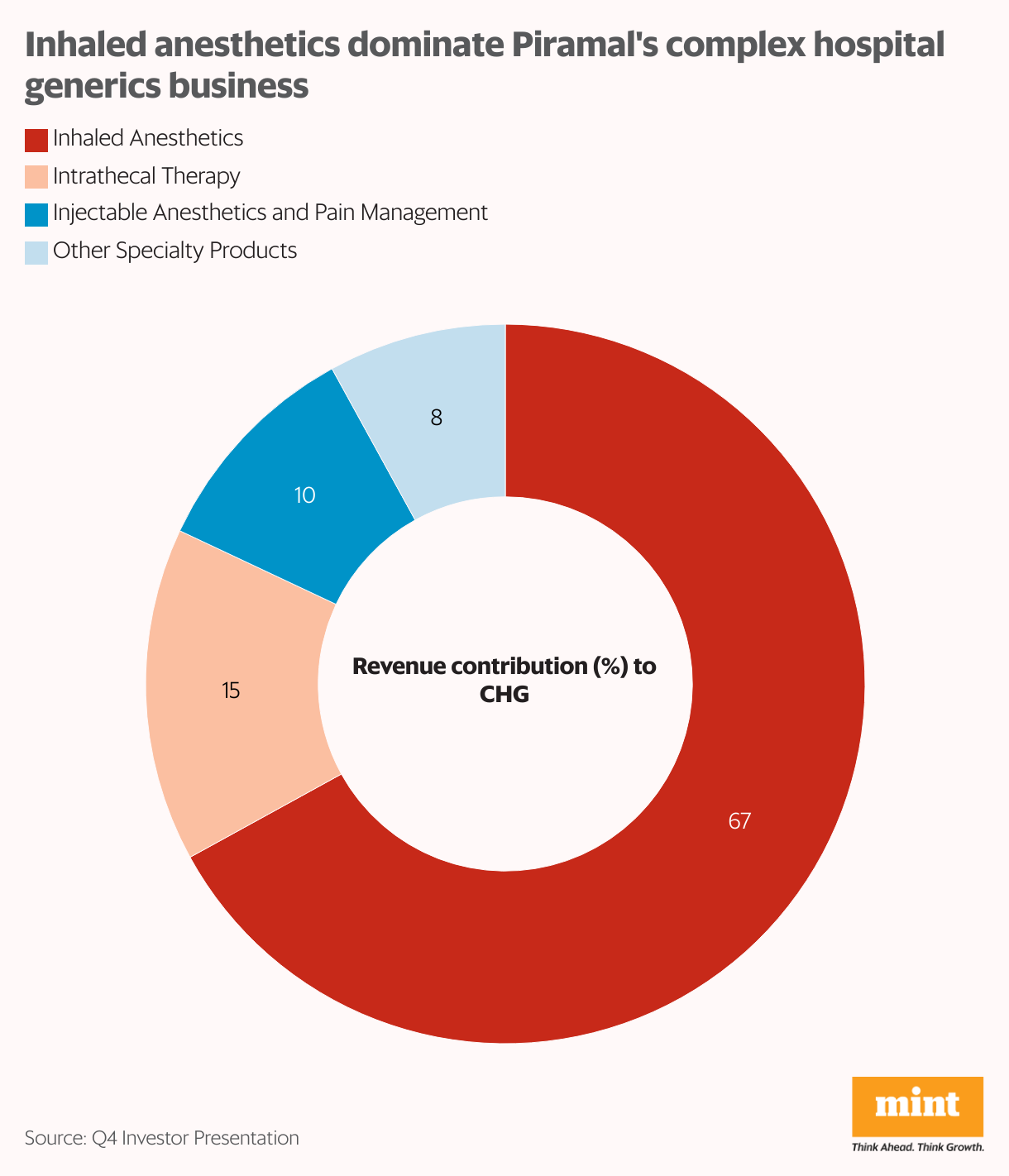

Piramal Pharma has also managed to hang on to its leading market share in its primary businesses—inhaled anesthetics and intrathecal therapy. It commands a 75% share of the US market in intrathecal baclofen, and a 44% share in inhaled anesthetics through the industry-leading ‘Sevoflurane’.

Sevoflurane accounts for 86% of the $1 billion global inhaled anesthetics market. Piramal Pharma plans to leverage its Sevoflurane facilities to try and capture the $400 million market for the drug outside the US and China.

Recent launches have further improved prospects for Piramal Pharma’s CHG business. In 2025, Piramal launched an injectable to treat psychiatric disorders, and has received commercialization rights for the neonatal cardiovascular drug ‘Neoatricon’. The management aims to grow the segment to $600 million by FY30.

CDMO pipeline propels hopes

To cater to rising US consumer demand, Piramal recently announced new capital expenditure worth $90 million in its US CDMO facilities at Lexington and Riverview. This should help it capture a larger share of antibody-drug-conjugates (ADCs) and injectables. The injectables market is projected at $20 billion by 2028.

The segment also boasts of 2.8x expansion in its development pipeline from 52 products in FY17 to 145 in FY25.

Another tailwind can come from the US Biosecure Act, which if approved will benefit Indian CDMOs by prohibiting imports of biotechnology equipment from China. Piramal’s management aims to grow its CDMO business to $1.2 billion by FY30.

Short-term volatility

Notwithstanding the near-term headwinds, Piramal has affirmed its FY30 outlook of $2 billion in revenue with 25% EBITDA margin and 1x net debt/EBITDA. Brokerages expect the company’s profit before tax (PBT) margin to expand to 16% by FY28.

But short-term volatility cannot be ruled out. Brokerages have slashed their price target for Piramal to a wide range from ₹230 to ₹340 per share. Introduction of futures and options (F&O) contracts on the counter at the end of this month can also add to the volatility.

At 2.45 pm on Monday, Piramal Pharma shares were up about 0.30% at ₹205.50 apiece, down from a 2% jump earlier in the day. Nifty Pharma was up about 0.70%.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.

Source:https://www.livemint.com/market/stock-market-news/piramal-pharma-market-correction-us-reciprocal-tariffs-trump-drug-price-order-generic-drugs-contract-manufacturing-11747641357789.html