With no experience in heading a large corporation, nor deep understanding of engineering, Anu Aga’s earnest efforts to steady the ship yielded little result in the face of the macroeconomic headwinds of the 1997 Asian financial crisis. The shares of the newly listed company more than halved in value between 1996 and 1998.

That’s when an anonymous shareholder letter arrived, which has since become a part of the Indian corporate folklore. The shareholder allegedly told Aga that she had let the shareholders down.

“Letting down, for us, is a dirty word. I couldn’t sleep,” Aga told Mint during a meeting last December, at Thermax’s head office in Pune.

She hired the Boston Consulting Group to script a turnaround. What followed is a well-documented reinvention story that is still referenced in business conferences and taught in management schools.

Cut to 2025. It’s time to make sulking shareholders happy again.

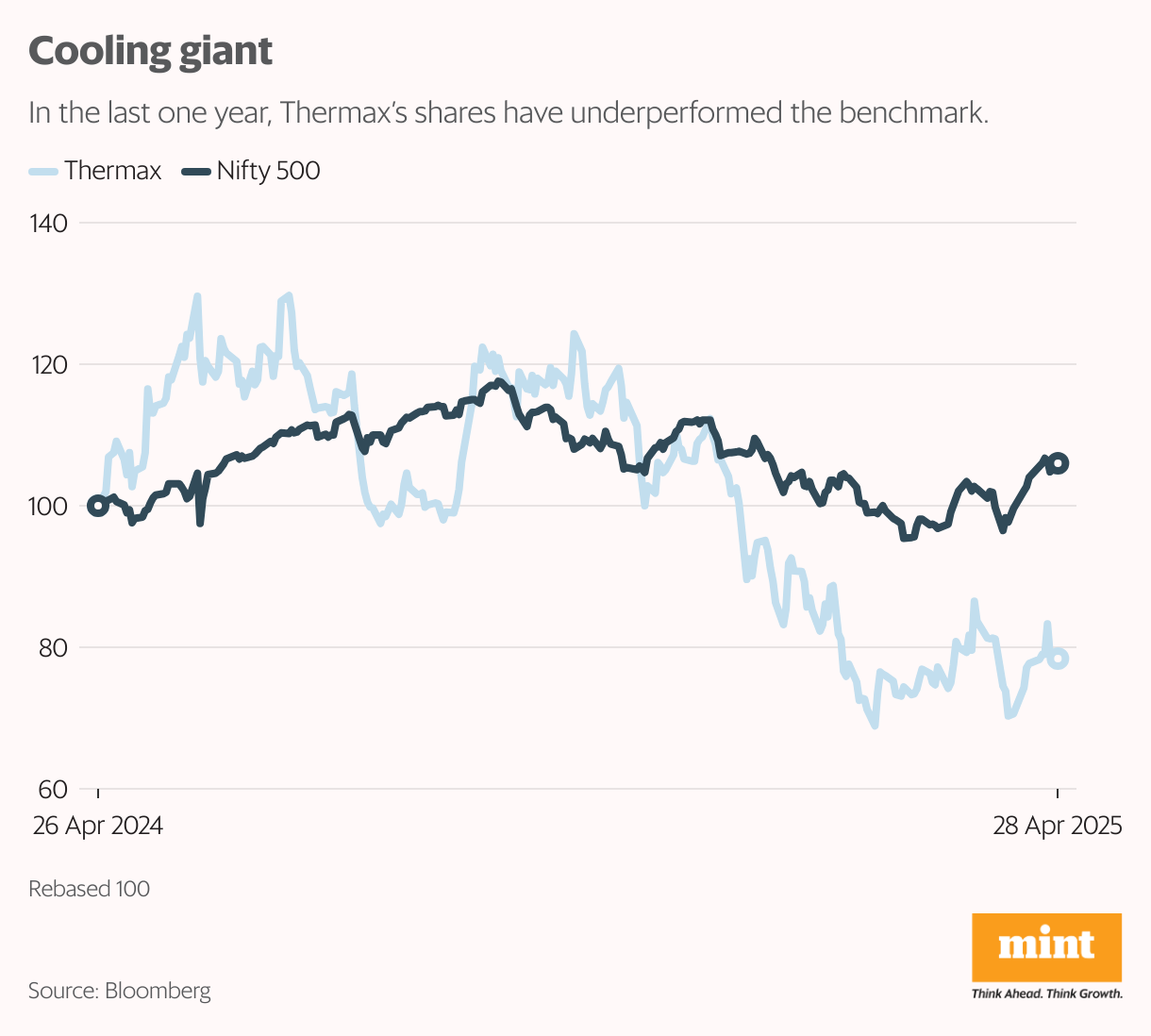

During the post-covid bull-run, as investors chased themes around sustainability, the conglomerate’s stock grew over five-fold between 2021 and 2024. It hit a 52-week high of ₹5,835 in July 2024. However, the stock has fallen over 40% since, and closed at ₹3416 on 28 April as growth slowed down to a crawling pace while losses mounted in its new ventures. Brokerages across the board have trimmed price targets. In this period, Thermax’s shares have also underperformed market index Nifty 500.

“The weakness in earnings in the past few quarters, and losses in large projects, have led to earnings downgrades and the stock correction. This period also coincided with a slowdown in private capex, so order growth for Thermax tapered. Due to this, the euphoric froth in the stock got washed away,” said Renu Baid Pugalia, senior vice president, research, at IIFL Institutional Equities, a brokerage.

The big questions: By when can the company turnaround its fortunes, cheering its shareholders yet again? And can the legacy company, known to be conservative, find its footing in a fast-changing economy?

New bets

Traditionally known for making industrial boilers (they produce steam for power needs, among other applications), Thermax has pegged its reinvention around energy transition and emissions reduction. From selling steam made from renewable energy to making industrial-scale biogas plants that offer a cleaner alternative to crop burning, the company, for the past five years, has been diversifying into several new businesses.

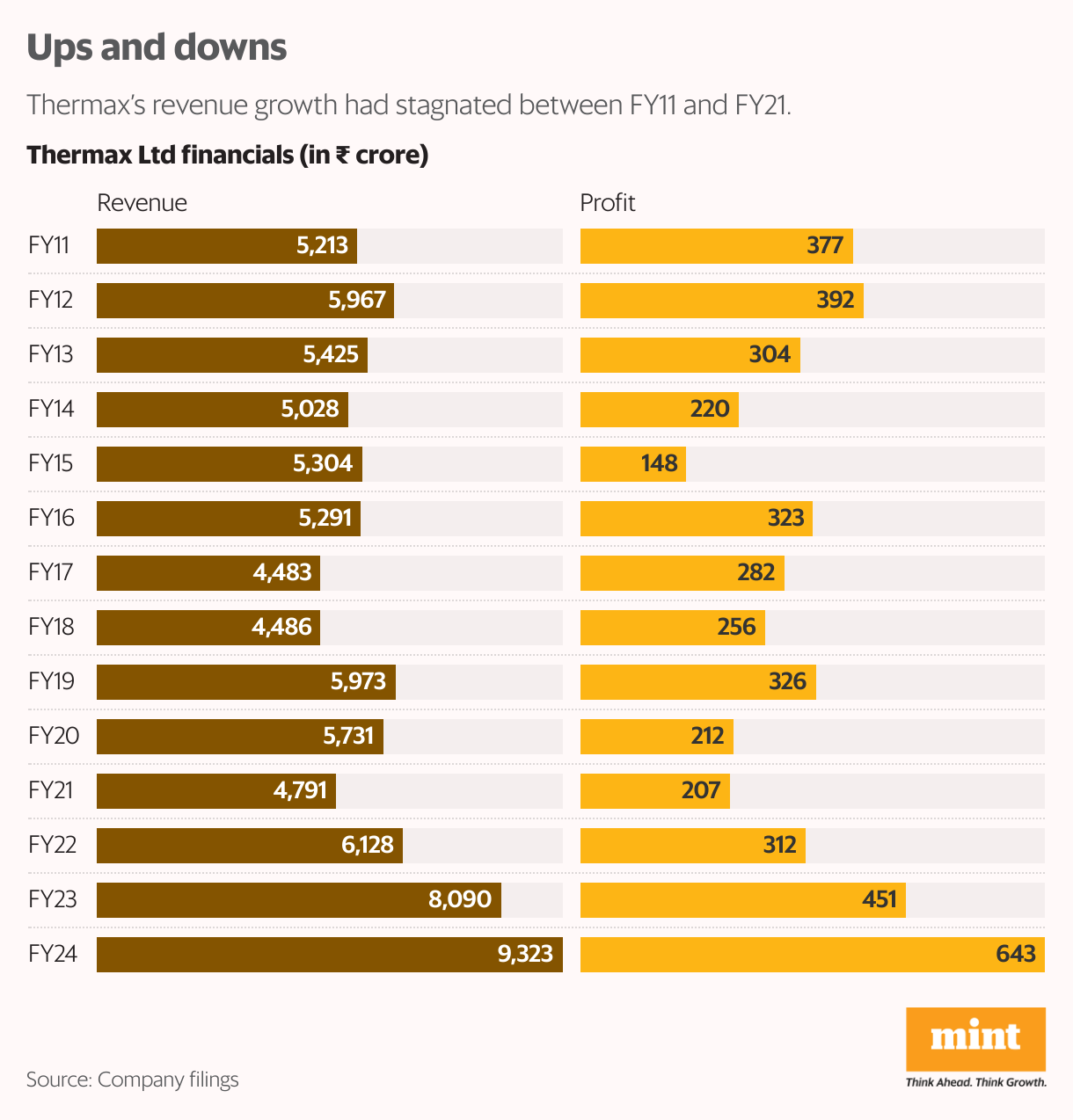

Thermax clocked sales revenue of ₹1,626 crore in FY06 with a profit of ₹103 crore. Revenue more than tripled by FY11 to ₹5,213 crore. There was a similar growth in profit over these five years to ₹377 crore.

But a decade later in FY20? Revenue stood at ₹5,731 crore. Profit declined to ₹212 crore. With stagnating revenue and declining profit, Thermax had to reinvent, or it risked obsolescence.

When M.S. Unnikrishnan, the long-term chief executive (CEO) and managing director (MD) of Thermax was retiring in June 2020, after 38 years at the company, the company opted for an outsider. Ashish Bhandari, the incumbent CEO and MD, was a career General Electric employee when he was hired in 2020.

Bhandari had his task cut out.

“Thermax was not growing. Things that got us here, were not going to get us ahead,” he said. “Meanwhile, a whole host of new opportunities were coming up, which, if we were able to capture, would create a future that was very exciting.”

At a board retreat in November 2021, the company chalked out a roadmap for the next decade. Thermax would bet on its domain expertise in the energy space and help customers in energy transitions. It set a target to triple its revenue to ₹18,500 crore by 2030, with more than half of that coming from new businesses incubated during the decade.

The company got deeper into the solutions business—offering steam, water or clean power as a service on a per unit basis. To be sure, it toyed with the idea of selling steam as a service more than 15 years ago, but only now has it started scaling the business. Thermax operates close to 50 plants on this ‘build-own-operate’ model. Other opportunities on the company’s radar include green hydrogen, advanced biofuels, supercritical boilers and carbon capture technologies.

However, capitalizing on new opportunities meant taking on risk and doing things differently than the company was used to, Bhandari said. For instance, the build-own-operate model meant taking on debt for the first time in years.

View Full Image

“I am more conservative and not a big risk taker. I would like our balance sheet not to be leveraged. So, if tomorrow Ashish (Bhandari) says there is a big opportunity, but it needs us to leverage our balance sheet, that would make me stay up at night,” said Meher Pudumjee, the non-executive chairperson of Thermax and daughter of Aga.

In typical Thermax fashion, the company insisted on keeping the debt limited to special purpose vehicles (SPVs) set up to own these assets, with no corporate guarantees from the parent company. “We expect these businesses to have their own financial models that are stable. We don’t want to subsidize the risk of an asset through Thermax. Every asset, every SPV, should be able to raise money, make its own business case,” Bhandari said.

Like Meher Pudumjee, her husband, Pheroz Pudumjee, also holds a non-executive board position. Their children have joined Thermax and are learning the ropes. Son Zahaan is executive assistant to the CEO, while daughter Lea is a product manager.

Zahaan Pudumjee, Meher Pudumjee, Pheroz Pudumjee, Anu Aga and Lea Pudumjee.")

View Full Image

No giga-scale promise

But Thermax’s conservative approach—its averseness to taking on debt, judicious pace of expansion, being picky about its customers and only entering businesses with a clear path to profitability—may put it at a disadvantage in a market that values snazzy headlines and giga-scale promises, experts said.

Case in point: First Energy Pvt Ltd (FEPL), which is part of Thermax’s green solutions portfolio. It supplies renewable electricity to industrial clients on a build-own-operate model. The client pays a flat tariff for the green power. Since its inception in 2021, the business has scaled to about 300 megawatts of renewable energy capacity.

The project is running behind schedule and is bleeding capital as Thermax treads at a judicious pace. Meanwhile, O2 Power, a renewable power platform set up by private equity investors EQT and Temasek in 2020, has managed to scale to 1.3 gigawatts of operational assets when it was acquired by a subsidiary of JSW Energy this year at an enterprise valuation of ₹12,468 crore. Other venture-capital backed renewable energy platforms have also scaled at a comparable pace, with investors making profitable exits in recent months.

For Thermax, land acquisition proved to be more difficult than anticipated. The returns from the business too weren’t what the company had expected. “In FEPL, we have had quite a few losses this year. We expect those losses to come down substantially next year, though even next year would be loss making…with breakeven the year after,” Bhandari said during an analyst call on 7 February.

Thermax has invested about ₹20 crore in equity and about ₹300 crore in debt in FEPL so far this fiscal, he said. The target is to invest another ₹500 crore to scale the business to 1 gigawatt capacity.

First Energy Pvt Ltd, which is part of Thermax’s green solutions portfolio, supplies renewable electricity to industrial clients on a build-own-operate model. It is running behind schedule and is bleeding capital.

Similarly, Thermax Bioenergy Solutions Pvt Ltd, part of Thermax’s industrial infra portfolio, has been haemorrhaging capital. It makes bio-compressed natural gas (CNG) plants that use agricultural waste as feedstock and offer a commercially viable alternative to crop burning.

Thermax has invested over ₹100 crore in the business in just the last one year as it struggles to translate its laboratory successes to industrial scale plants. However, it booked this investment as a revenue expense rather than a research and development spend that can be capitalized on the balance sheet and amortized over a longer period. This means a hit on the company’s financials in the short term—and unhappy investors.

Growth pangs

Apart from green solutions and industrial infra, Thermax operates in two other segments—industrial products and chemicals. However, industrial products and industrial infra account for about 85% of the company’s revenue and a similar share of its profit.

The industrial products segment, which includes the sale of boilers, heaters, waste heat recovery systems, air and water purification systems, has been going strong. Its revenue grew 9% year-on-year for the first nine months of FY25 to ₹3,099 crore, with ₹323 crore in profit before interest and tax (PBIT). PBIT margin expanded 1.4 percentage points to 10.4%.

The industrial infra segment, which houses several engineering, procurement and construction (EPC) businesses, is where the company is facing a challenge. Revenue grew 6% to ₹3,299 crore during the first nine months. But new orders have dried up while cost overruns in existing projects led to PBIT margins halving to a measly 2.2% in the first nine months.

The segment’s order inflow halved during the October-December quarter compared to the preceding year to ₹669 crore, dragging the company’s consolidated order booking during the quarter down by nearly a tenth, despite a healthy growth in the industrial products segment.

“It was a difficult quarter, and the results were below our expectations,” Bhandari said in the analyst call on 7 February. “That said, I expect a strong quarter 4, potentially even a very strong quarter 4,” he stressed.

But as Thermax takes on debt to fund the build-own-operate steam projects, it also changes the nature of its balance sheet, which has historically been flush with cash, said Amit Anwani, vice president and lead analyst for capital goods, industrials and defence at Prabhudas Lilladher Pvt Ltd, a brokerage.

“The steam supply business, where Thermax does the capital investment, exposes the company’s balance sheet to the business cycles of its customers. It is also investing in solar power generation assets. Historically, these businesses take a lot of time to firm up and give returns,” he said.

What is also not helping Thermax’s case is that its Ebitda margins have remained range bound between 7.5-8.5%, Anwani said, adding that the market had priced in higher margins. Meanwhile, there has been an execution and order intake challenge. The company’s book-to-bill ratio—a measure of its order book versus trailing-twelve-months revenue—is at a measly 1.1, indicating lower growth, he said. “All this is reflected in the stock price correction.”

Time to execute

IIFL’s Pugalia is unconvinced by Thermax’s efforts to reinvent itself. Her premise: Thermax is not really about ‘projects’; it is a ‘products’ company.

“They (Thermax) do not have the DNA to execute projects. Somewhere or the other, they go wrong on execution, cost estimation, etc,” she said.

In other words, solutions such as steam as a service, where the company first leverages its balance sheet to build the solution and then sell it as a service, isn’t really its forte. In the late 2000s, Thermax struggled to execute utility scale boiler projects, Pugalia said. Then the company faced challenges executing large captive power projects, flue-gas desulphurization projects and now, the bio-CNG plants and refinery projects.

“Every company has an inherent strength. Thermax’s strength lies in products. In a sense, how they get over this is the test of how they evolve,” she said.

Kavil Ramachandran, professor of family business and entrepreneurship at the Indian School of Business, recently co-authored a case study on Thermax. He said that while the company’s financials will take short-term hits as it transitions, its performance must be benchmarked over longer horizons.

View Full Image

“The long-term investments will pay off only when the performance is not measured quarter to quarter or by stock price. The problem with many companies is that a CEO is judged by profits or stock price,” he said.

Moreover, Thermax is in the renewable energy sector, where changes are not as rapid, compared to a sector like electronics, Ramachandran added. This allows the company the liberty to be conservative with its investments. “Not to run, versus not knowing how to run, are two different things,” he further said.

Thermax knows to run but investors would like the company to win the race.

Source:https://www.livemint.com/companies/thermax-steam-renewable-energy-anu-aga-meher-pudumjee-shareholder-investors-revenue-margins-11745840686686.html