Insurance is not only a legal requirement, but it also serves as a strategy to mitigate financial risk in the presence of unforeseen damages and liabilities. One type of car insurance policy that has become increasingly popular in recent years is known as Zero Dep Car Insurance, Zero Depreciation Car Insurance, or Bumper-to-Bumper Insurance. In this blog, we shall focus on explaining what Zero Depreciation Car Insurance is, its benefits, key features, and if it is the right choice for you or not. It offers complete information for car owners seeking to protect their vehicles and mitigate expenses when paying for unplanned accidents.

What is Zero Depreciation Car Insurance?

Understanding Zero Dep Car Insurance requires some background knowledge of standard car insurances. When you make a claim with the insurance company for accident-related repairs or vehicle replacement, your insurance company will account for the depreciation of the vehicle’s parts. In other words, you receive payment for the reduced value of the parts, not their original price. This practice can lead to significant expenses incurred by the car owner, especially when expensive parts like bumpers or headlights are involved, seeing as insurance companies will not cover the full value of the components.

Unlike regular policies, Zero Dep Car Insurance enables one to retain full coverage and protection without depreciation. This means your claim will be fully reimbursed which allows you to incur little to no out-of-pocket expenses when car parts need to be replaced. You will appreciate this policy if you prefer assurance and low-stress encounters regarding the repairs needed after an accident.

Highlights of Zero Depreciation Car Insurance

- Full Claim Settlement: The unique feature is the full payment of the depreciation free repair and replacement costs. Meaning, hidden costs associated with a standard policy, with no depreciation with settlement claims, can be avoided because you will have the invoice value of the parts replaced during the claims.

- Covers Fiber, Plastic, and Metal Parts: Other than standard policies, foam, fiberglass and plastic parts which are more susceptible to damages are also included in the Zero Dep Car Insurance coverage. Modern cars typically use these materials, and if they are not fully insured, they can be costly to replace.

- Usually for New Cars: Zero Dep Car Insurance is offered by most insurers for cars which are up to 5 years old. This policy is restricted to new cars because the newer vehicles has higher part value, and the owners are likely to keep the cars well maintained so these parts will be in good condition.

- Limited Claims Per Year: A number of insurers impose restrictions on the amount of Zero Dep claims that can be made in a year. It is good to note these restrictions so they can budget their claims appropriately for the duration of the coverage.

- Addition Policy: Usually, this comes as an addition to the car coverage insurance. Even though it’s not a separate item, it considerably improves the worth of a basic policy by increasing coverage range.

- More Expensive Premiums: The greater part of the policy has more details; hence the premiums tend to be slightly more expensive. This extra charge, however, is worth the amount of protection and the ease it provides when settling claims.

Must Read: Health Insurance Plans For Family

Benefits of Zero Depreciation Car Insurance

-

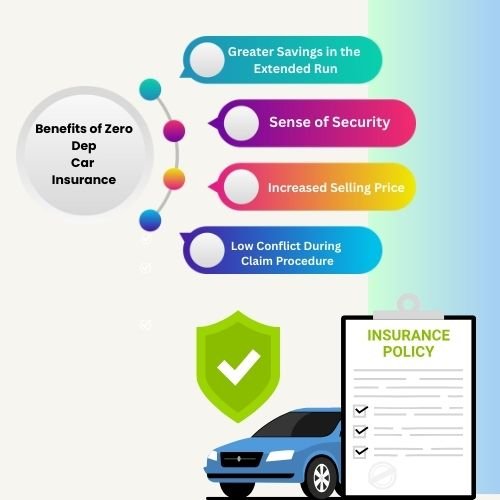

Greater Savings in the Extended Run

Even though Zero Depreciation Car Insurance needs a higher premium, it greatly lessens the out-of-the-pocket value at the time when a claim is made. For luxurious vehicles, the repair costs can be extraordinarily high. This sort of insurance makes sure that such costs do not burden the policyholder. For car owners who seek complete protection, these savings can outnumber the additional premium over time, turning it into a wise decision.

-

Sense of Security

It is greatly reassuring to know that your policy encompasses defects without any deduction for depreciation. You can drive without worries and have your peace of mind knowing you’re covered. This is particularly useful in traffic or city settings where the chances of minor scratches and damage are much higher compared to the countryside.

-

Increased Selling Price

Unlike other motor vehicles, those that have been serviced with a Zero Dep Car Insurance policy are after-market serviced items for which the service history does not contain excessive fleet costs, thereby increasing its resale value. The market value of the vehicle increases because buyers prefer a well-kept vehicle with comprehensive insurance that increases its maintenance credibility.

-

Low Conflict During Claim Procedure

Leaving out depreciation tends to leave the value of parts in dispute lower, which results in less conflict for claims, ensuring quicker claims processing. This contributes to the faster processing of return for the vehicle after adjustments with lesser time and complications.

-

Superior Safeguards for High Value Parts

Components such as alloy wheels, bumpers, and headlights can be very costly to replace. For luxury and high-end vehicles, Zero Dep Car Insurance is ideal because it ensures these parts are covered fully. It eliminates the need to worry about unexpected repair bills and ensures that original parts are used without any extra costs.

Must Read: LIC Tech Term Plan

Who Should Select Zero Depreciation Car Insurance?

- Newly Joined Employees: Misplacing a company asset, such as a laptop, bounding with the features becomes expensive with the latest devices. Zero Dep coverage is beneficial for them as it provides peace of mind and helps avoid unexpected repair bills.

- First Time Buyers: Those who are new to the concept of car maintenance and part pricing due to lack of experience will find it easier thanks to Zero Dep coverage since they would not worry about the stress of hidden pay repairs.

- Suburban Motorists: Driving and often brings more chances of minor collisions. This policy suits frequent suburban motorists. Along with slow moving traffic and little-free parking spots, minor dents and scrapes are more than usual and are all insured under Zero Dep.

- Owners of Luxury Vehicles: Zero Dep coverage car insurance is ideal for people with expensive cars, as the benefits are higher. For high-end cars, protecting high-value parts with Zero Dep coverage helps retain the car’s condition, value, and investment.

- Young/Novice Drivers: Younger drivers tend to be less careful, meaning they’ll likely get into accidents; Zero Dep makes sure they bear no financial burden. It gives them the opportunity to learn and gain experience without the stress of repair expenses from small accidents.

What Does Zero Depreciation Car Insurance Cover?

- Accidental damages to the car

- Repair and replacement of depreciable parts

- Damages due to natural calamities (if included in the base policy)

- Man-made disasters like riots or vandalism (if included in the base policy)

- Fiberglass, plastic, and metal component repairs

- Full replacement value of parts without any depreciation deduction

What’s Not Covered?

- Accident free mechanical and electrical breakdowns

- Driving while intoxicated (DWI)

- Excess claims within the stipulated period

- Indicated private vehicle uses for commercial purposes other than what is mentioned in the endorsement.

How to Buy Zero Depreciation Car Insurance

- Check Eligibility: Check if your vehicle is the eligible one. Sometimes cars older than 5 years might also be accepted so check with the insurer.

- Check Competitors: Aggregators might produce an optimal solution in their offers. Be it purchase price or available features the offer for the car could be the most comprehensive.

- Selecting Suitable Optional Covers: While purchasing Zero Dep, think of additional features like engine guard or roadside help. These features may further improve the policy’s value for you.

- Assess the Policy Terms: Determine the limit on the number of allowed claims, coverage gaps, and individual claim specifics. Assessing these considerations helps not having surprises during the claim process.

Claim Steps for Car Insurance Zero Depreciation

- Notify the Insurance Provider Without Delay: Notify your insurer as soon as the accident occurs. Early notice can ensure that there are no hurdles in registering the claim.

- Survey and Inspection: The insurer’s surveyor will evaluate the damage. They will evaluate the loss and decide whether it exceeds the Zero Dep deductible.

- Garage Tie-Up: Have your vehicle repaired at a network garage. Network garages would likely have a quicker payment process which would make reimbursement easier.

- Claim Payment: The insurer will settle the claim after the policyholder submits and reviews all supporting documents. There is no need for the policyholder to make direct payments and sign back claim waivers.

Zero Depreciation Car Insurance Cost

The premium associated with Zero Depreciation Car Insurance is usually 15-20% more expensive than a comprehensive policy. The additional premium is offset by lower out-of-pocket expenses incurred during claims. Savings from out-of-pocket expenses can add up significantly over the lifetime of the vehicle, particularly if several repairs are needed.

Best Practices for Selecting Zero Depreciation Car Insurance

Confirm Claim Limits: Some policies limit Zero Dep claims to a maximum of 2 per year. This information helps the user plan for the most financially advantageous use of the benefit.

Clearly Understand Inclusions and Exclusions: Make sure the policy entails all major parts relevant to the insured and other possible scenarios related to their driving habits.

Verify Insurer’s Claim Settlement Ratio: The ratio defines how reliable the insurer is. Higher ratios increase the chance of the claimant being granted approval for the claim.

Use No-Cost Yard Services: Choose insurers with a wide range of no-cost yard services. This simplifies the repair and claim processes.

Review Customers’ Feedback: Reviews do indicate actual customers’ experiences. They help uncover issues or benefits outside the policy’s explicit terms that may not have been clearly outlined.

Must Read: Term Insurance Plans for 70 year old in India

Common Misconceptions about Zero Depreciation Car Insurance

Myth 1: It Covers Every Possible Damage

Not quite. Policies that arise out of criminal acts or driving under the influence are not covered. It is better to be well-informed about a policy’s exclusions in order to avoid surprises when it comes to the claims process.

Myth 2: It’s Too Expensive to Be Worth It

The premium is higher, but the long-term savings during claims have the potential to far exceed the extra expense. In cases where several small accidents occur, this add-on pays for itself during the policy period more often than not.

Myth 3: It’s Only for Luxury Cars

This is untrue. Even mid-range cars stand to benefit from Zero Dep Car Insurance. Vehicle owners who desire greater protection along with added peace of mind will appreciate this type of insurance, irrespective of whether their vehicle is luxury or mid-range.

Conclusion

For those seeking maximum protection of their vehicles, Zero Depreciation Car Insurance is the solution. Greater peace of mind, lesser out-of-pocket expenses, and a more streamlined claims process are a few of the advantages that come with higher premiums. This insurance supports expensive new cars or cars that are used often, because it covers the full repair cost, not the depreciated value. It enables car owners to effortlessly enjoy vehicle ownership by alleviating the financial burden associated with maintaining the car in good shape.

If you are someone who prefers planning carefully or someone who wants to avoid the financial burden that could arise from accidents, buying a Zero Dep Car Insurance policy for your car might be one of the best decisions you make regarding car ownership. It is a smart, forward-thinking choice that ensures jolts to your vehicle and expenses are well managed for the long-term.

FAQs About Zero Depreciation Car Insurance

Q1: Is Zero Dep Car Insurance available for all vehicles?

A: No, generally it is for cars less than 5 years. However, some insurers offer it for older vehicles, though at a steeper price.

Q2: Is it possible to change my current policy to a Zero Dep Car Insurance?

A: Yes, if your insurer permits it, you can select it as an add-on during renewal.

Q3: What is the limit on the number of claims that can be made under Zero Dep Car Insurance?

A: Under Zero Dep feature, most policies permit 1-2 claims in a year, however this varies with different insurers.

Q4: Is the damage to the engine covered under Zero Dep Car Insurance?

A: Only if engine protection is added as an extra rider.

Q5: Is it compulsory to have Zero Dep Insurance?

A: It is not mandatory, but strongly suggested for new cars or high-end vehicles.

Q6: If I have No Claim Bonus (NCB), will my premium decrease?

A: Yes, NCB benefits still apply even if you have a Zero Dep add-on.

Q7: Does the IDV (Insured Declared Value) increase with Zero Dep Car Insurance?

A: No, the IDV stays the same, and is only impacted by the claim settlement, not the insured value of the vehicle.